by Jon S | Nov 1, 2022 | Education

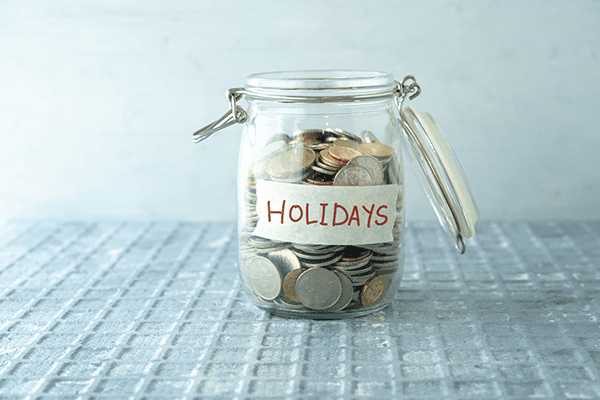

The holidays have officially arrived and with them—holiday spending! We all want to show our loved ones how much we care through gifts, festive meals, and fun activities (skiing, we’re looking at you), but if we’re not careful, we can really rack up our spending. Even...

by Jon S | Aug 16, 2022 | Education

It’s no secret that interest rates are rising. After experiencing record-low rates in 2020 and 2021, they were bound to go back up! And if you’re a consumer (hint: we all are) then these rising interest rates will affect some part of your financial situation in the...

by Jon S | Jul 26, 2022 | Education

There’s only one certainty in life: change. And you don’t need to be a financial expert to see that the current changing market directly affects all of us. We can see it in the prices of our gas and groceries, electronics and vehicles, and in our rent and mortgages....

by Jon S | May 25, 2022 | Education

Congratulations! You’re ready to start that home project you’ve been dreaming about. The only problem? Funds. Building projects don’t come cheap, especially when done correctly. So how do you finance constructing your home, expanding with an addition, undertaking a...

by Jon S | May 9, 2022 | Education

We understand—life happens and you go over your budget. Other times unforeseen circumstances may put you in a vulnerable financial situation. It’s okay. You’re not alone and it is possible to be in control again. Be kind to yourself during these uncertain times. If...

by Jon S | Aug 12, 2021 | Education

Is Saving Money Truly Important? Yes, saving money is truly important! According to a 2019 Bankrate survey, a mere 18% of Americans have six months’ worth of living expenses saved? While many factors contribute to individuals not saving, we believe that we can empower...